Managing money in India can feel like a juggling act. With rising costs, family responsibilities, and dreams of financial security, it’s easy to lose track of where your income goes. The 50-30-20 rule offers a simple, effective way to organize your finances, ensuring you cover essentials, enjoy life, and save for the future.

This budgeting method, popularized by U.S. Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. In this comprehensive guide, we’ll explore how to apply the 50-30-20 rule in India, its benefits, challenges, and practical tips to make it work for you.”50-30-20 Rule: Best Way to Manage Your Income”

Table of Contents

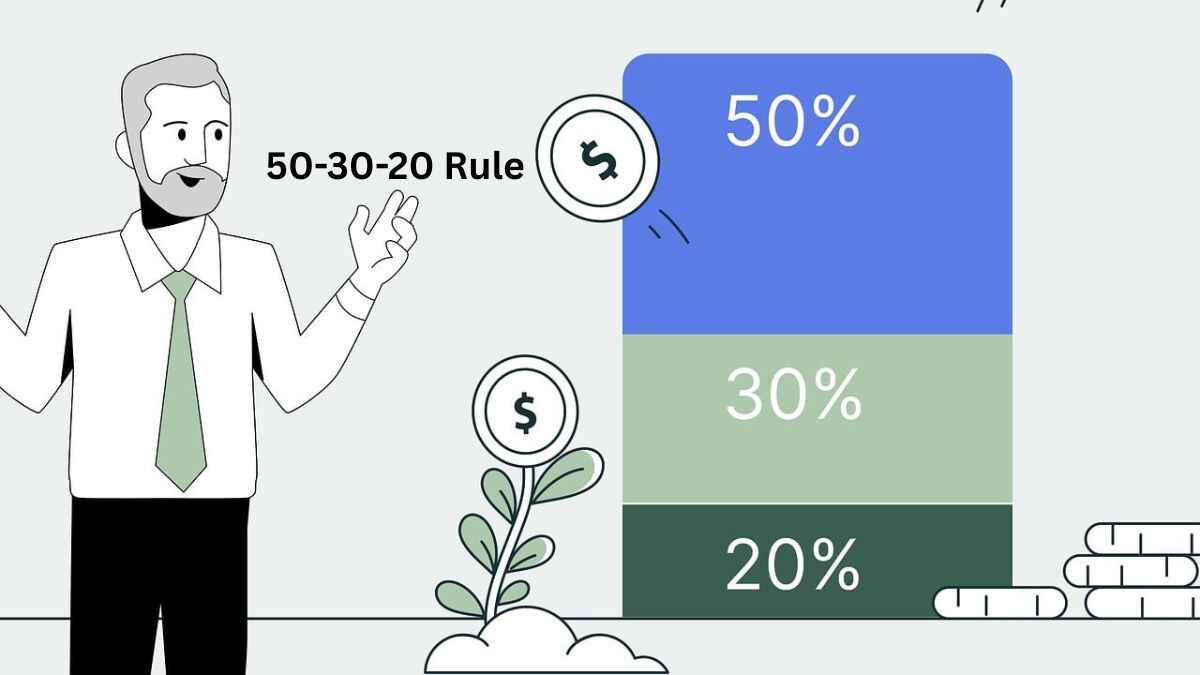

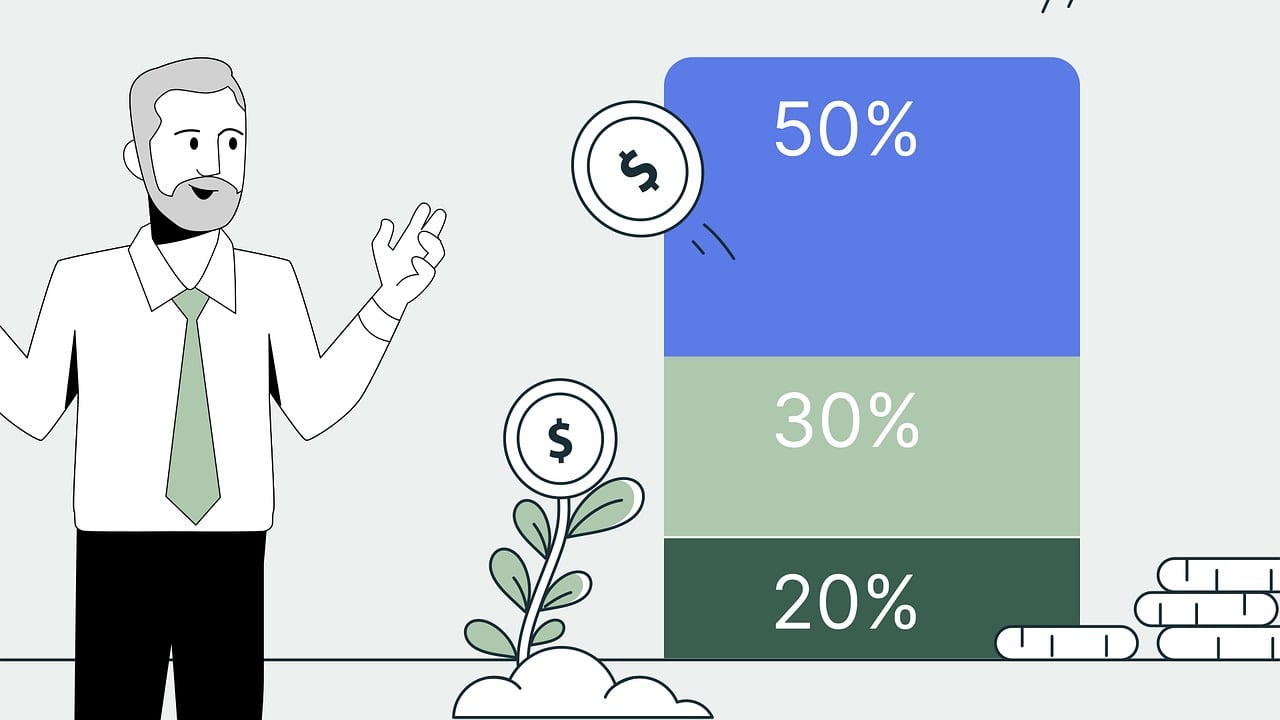

What Is the 50-30-20 Rule?

The 50-30-20 rule is a budgeting framework that helps you allocate your monthly after-tax income into three broad categories:

- 50% for Needs: Essential expenses required for survival, such as rent, groceries, and utilities.

- 30% for Wants: Discretionary spending that enhances your lifestyle, like dining out or travel.

- 20% for Savings and Debt Repayment: Money set aside for emergency funds, investments, or paying off debts beyond the minimum required.

This method is intuitive and flexible, making it ideal for Indians navigating diverse financial landscapes, from metropolitan cities with high living costs to smaller towns with modest expenses. By following the 50-30-20 rule, you can achieve a balance between meeting immediate needs, enjoying life, and building long-term financial security.

Why the 50-30-20 Rule Matters in India

India’s economic environment is unique, with varying income levels, inflation rates, and cultural expectations like supporting extended families or funding festivals. The 50-30-20 rule is particularly relevant because it:

- Simplifies Budgeting: Its straightforward percentages make it easy to follow, even for those new to financial planning.

- Promotes Balance: It ensures you enjoy life while saving for goals like buying a home, funding education, or planning retirement.

- Adapts to Circumstances: The rule can be adjusted for high-debt situations, low incomes, or irregular earnings, which are common in India.

Whether you’re a salaried professional in Mumbai, a freelancer in Bengaluru, or a small business owner in a Tier-2 city, the 50-30-20 rule provides a practical framework to manage your income effectively.

Breaking Down the Components

Let’s dive into the three categories of the 50-30-20 rule and how they apply in the Indian context.

1. Needs (50%)

Definition: Needs are essential expenses required for basic living and functioning. These are non-negotiable costs you can’t avoid.

Examples in India:

- Rent or home loan EMIs (e.g., ₹20,000 for a 1BHK in a metro city)

- Groceries and household essentials (e.g., ₹6,000 for a family of four)

- Utility bills (electricity, water, internet, gas)

- Transportation (fuel, public transport like metro or bus, or vehicle maintenance)

- Health insurance premiums

- Minimum debt repayments (e.g., credit card minimums or loan EMIs)

- Childcare or education fees (e.g., school fees or coaching classes)

Why It Matters: Allocating 50% of your income to needs ensures your basic requirements are met, providing a stable foundation for your budget. In India, where housing and food costs can be significant, prioritizing needs prevents financial strain.

Tip: If your needs exceed 50%, consider cost-saving measures like moving to a more affordable area, sharing accommodations, or switching to cheaper utility plans.

2. Wants (30%)

Definition: Wants are discretionary expenses that enhance your lifestyle but aren’t essential for survival. These are things you enjoy but could live without if necessary.

Examples in India:

- Dining out or ordering food (e.g., weekend meals at restaurants)

- Entertainment (movies, streaming services like Netflix or Amazon Prime)

- Gym memberships or fitness classes (e.g., yoga or Zumba)

- Travel and vacations (e.g., a weekend getaway to Goa)

- Shopping for non-essential items (clothes, gadgets, accessories)

- Hobbies (e.g., photography, music lessons, or sports equipment)

Why It Matters: The 50-30-20 rule allows 30% for wants, ensuring you can enjoy life without guilt. In India, where social and cultural activities like festivals or family outings are important, this category helps maintain a balanced lifestyle.

Tip: Differentiate between needs and wants carefully. For example, a basic phone plan is a need, but a premium streaming subscription is a want. Review your spending to avoid overspending in this category.

3. Savings and Debt Repayment (20%)

Definition: This category includes money set aside for emergency funds, retirement, investments, and paying off debts beyond the minimum required.

Why It Matters: Saving 20% of your income builds a financial safety net and supports long-term goals. In India, where many lack adequate savings, this category is crucial for financial security.

Investment Options in India:

| Investment Type | Description | Benefits |

|---|---|---|

| Fixed Deposits (FDs) | Safe, low-risk investments with guaranteed returns | Up to 7.30% p.a. for senior citizens (e.g., Bajaj Finance FDs) |

| Public Provident Fund (PPF) | Government-backed, tax-saving scheme | Long-term savings with tax benefits under Section 80C |

| National Pension System (NPS) | Retirement-focused investment | Tax benefits and pension planning |

| Mutual Funds (SIPs) | Diversified investments through Systematic Investment Plans | Potential for higher returns, suitable for long-term goals |

| Real Estate Investment Trusts (REITs) | Invest in real estate without buying property | Diversification and passive income |

| Alternative Investment Funds (AIFs) | High-risk, high-return options | Suitable for experienced investors |

Tip: Automate savings by setting up auto-debits to a separate savings account or investment plan on payday. This ensures consistency and reduces the temptation to spend.

How to Apply the 50-30-20 Rule

Implementing the 50-30-20 rule is straightforward but requires some initial effort. Here’s a step-by-step guide tailored for India:

- Calculate Your After-Tax Income

Determine your monthly take-home pay after taxes and deductions (e.g., income tax, provident fund). For example, if your gross salary is ₹60,000 and deductions are ₹10,000, your after-tax income is ₹50,000. - Track Your Expenses

Record all expenses for one to two months to understand your spending patterns. Use apps like Moneycontrol or Walnut, or simply maintain a spreadsheet. Categorize expenses into needs, wants, and savings. - Categorize Your Expenses

Assign each expense to one of the three categories:- Needs: Rent, groceries, utilities

- Wants: Dining out, entertainment

- Savings: Emergency fund, investments, extra debt payments

- Allocate Your Income

Divide your after-tax income according to the 50-30-20 rule:- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

- Automate Your Savings

Set up automatic transfers to savings accounts, FDs, or SIPs on payday. For example, if you earn ₹50,000, transfer ₹10,000 (20%) to a savings or investment account immediately. - Review and Adjust

Review your budget monthly to ensure you’re staying within the allocated percentages. Adjust for changes like a salary hike, new expenses, or life events (e.g., marriage or childbirth).

Example Allocation for ₹50,000 Monthly Income:

| Category | Percentage | Amount | Examples |

|---|---|---|---|

| Needs | 50% | ₹25,000 | Rent (₹15,000), Groceries (₹5,000), Utilities (₹2,000), Transport (₹2,000), Insurance (₹1,000) |

| Wants | 30% | ₹15,000 | Dining out (₹3,000), Entertainment (₹2,000), Shopping (₹5,000), Travel (₹5,000) |

| Savings | 20% | ₹10,000 | Emergency fund (₹3,000), SIPs (₹4,000), Debt repayment (₹3,000) |

Benefits of the 50-30-20 Rule

The 50-30-20 rule is popular because it offers several advantages, especially for Indian households:

- Simplicity: The rule’s clear percentages make it easy to understand and apply, even for beginners.

- Financial Discipline: It helps prioritize essential expenses and limits overspending on wants.

- Balanced Approach: It allows you to enjoy life while saving for the future, reducing financial stress.

- Flexibility: The rule can be adjusted to suit individual circumstances, such as high rent or significant debt.

Real-Life Examples in India

Here are two examples showing how the 50-30-20 rule can be applied to different income levels:

Example 1: Priya, Monthly Income ₹50,000 (Salaried Professional in Delhi)

- Needs (50%): ₹25,000

- Rent: ₹15,000

- Groceries: ₹5,000

- Utilities: ₹2,000

- Transportation: ₹2,000

- Insurance: ₹1,000

- Wants (30%): ₹15,000

- Dining out: ₹3,000

- Streaming subscriptions: ₹1,000

- Shopping: ₹5,000

- Weekend trips: ₹6,000

- Savings (20%): ₹10,000

- Emergency fund: ₹3,000

- Mutual fund SIP: ₹4,000

- Credit card repayment: ₹3,000

Example 2: Rahul, Monthly Income ₹1,50,000 (IT Professional in Bengaluru)

- Needs (50%): ₹75,000

- Home loan EMI: ₹40,000

- Groceries: ₹10,000

- Utilities: ₹5,000

- Transportation: ₹5,000

- Insurance: ₹5,000

- Childcare: ₹10,000

- Wants (30%): ₹45,000

- Dining out: ₹10,000

- Entertainment: ₹5,000

- Shopping: ₹10,000

- Travel: ₹10,000

- Hobbies: ₹10,000

- Savings (20%): ₹30,000

- Emergency fund: ₹5,000

- Retirement fund (NPS): ₹10,000

- Mutual funds: ₹10,000

- Extra loan repayment: ₹5,000

Common Mistakes and How to Avoid Them

While the 50-30-20 rule is effective, here are common pitfalls and solutions:

- Overspending on Wants

- Mistake: Spending more than 30% on wants, leaving less for savings.

- Solution: Track spending using apps or a notebook and cut back on non-essentials like frequent dining out.

- Neglecting Savings

- Mistake: Skipping the 20% savings allocation or using it for emergencies without replenishing.

- Solution: Automate savings transfers and treat them as a fixed expense.

- Not Reviewing the Budget

- Mistake: Failing to adjust the budget as income or expenses change.

- Solution: Review your budget monthly and after major life events like a job change or marriage.

Flexibility of the 50-30-20 Rule

The 50-30-20 rule is a guideline, not a strict rule. You can adjust the percentages based on your circumstances:

- High Debt: Allocate more than 20% to debt repayment to reduce interest costs faster.

- Low Income: If needs exceed 50%, reduce wants or explore ways to increase income (e.g., side gigs).

- High Income: Save more than 20% to accelerate goals like early retirement or buying a home.

Adjusted Example: If Priya’s rent increases to ₹20,000, her needs may rise to 60% (₹30,000). She could adjust to a 60-20-20 rule, reducing wants to ₹10,000 and keeping savings at ₹10,000.

Investment Strategies for the Savings Portion

The 20% savings portion is critical for building wealth. Here are some investment options tailored for India:

| Investment Option | Risk Level | Ideal For | Example Providers |

|---|---|---|---|

| Fixed Deposits | Low | Emergency funds, short-term goals | Bajaj Finance, SBI |

| PPF | Low | Tax-saving, long-term savings | Post Office, Banks |

| NPS | Moderate | Retirement planning | LIC, HDFC Pension |

| Mutual Funds (SIPs) | Moderate to High | Wealth creation | SBI Mutual Fund, ICICI Prudential |

| REITs | Moderate | Real estate exposure | Embassy REIT, Mindspace REIT |

Pro Tip: Use online calculators like those offered by Bajaj Finserv to estimate returns on FDs or SIPs.

Tips for Success in India

- Leverage Digital Tools: Use apps like Moneycontrol, ET Money, or Google Sheets to track expenses and investments.

- Account for Cultural Expenses: Budget for festivals, weddings, or family support within the wants or needs category.

- Start Small: If saving 20% feels overwhelming, begin with 10% and gradually increase as you adjust your spending.

- Seek Professional Advice: Consult a financial advisor for personalized investment strategies, especially for high-risk options like AIFs.

FAQs

Is the 50-30-20 rule suitable for everyone?

Yes, it’s a flexible guideline that can be adapted to most financial situations. However, those with high debt or low income may need to adjust the percentages.

What if my needs exceed 50% of my income?

Reduce spending on wants, explore cost-saving measures (e.g., cheaper housing), or increase income through side hustles.

Can I adjust the percentages based on my goals?

Absolutely. For example, you might use a 50-20-30 rule to save more or a 60-20-20 rule if needs are higher.

How do I handle irregular income?

Average your income over several months and base your budget on that average. Adjust as income fluctuates.

What if I have no debt?

Allocate the entire 20% to savings and investments, or use part for goals like buying a home or funding education.

How often should I review my budget?

Review monthly or after major life changes (e.g., job switch, marriage) to ensure the 50-30-20 rule aligns with your needs.

Conclusion

The 50-30-20 rule is a powerful tool for managing your income in India’s dynamic economic landscape. By allocating 50% to needs, 30% to wants, and 20% to savings and debt repayment, you can achieve a balance between enjoying the present and securing your future. Its simplicity and flexibility make it accessible to everyone, from young professionals to families.

To get started, calculate your after-tax income, track your expenses, and apply the 50-30-20 rule. Automate savings, review your budget regularly, and adjust as needed. With consistency and discipline, this budgeting method can transform your financial health, helping you achieve goals like building an emergency fund, investing for retirement, or enjoying life’s pleasures without guilt.

For more resources, explore investment options at Grip Invest, Ujjivan Small Finance Bank, or Bajaj Finserv. Start your budgeting journey today and take control of your financial future!

Disclaimer: Moneyjack.in provides general financial information for educational purposes only. We are not financial advisors. Content is not personalized advice. Consult a qualified professional before making financial decisions. We are not liable for any losses or damages arising from the use of our content. Always conduct your own research.